Fair Value Of Loans Ifrs 9

Disclosure of information about the fair value of the collateral and other credit enhancements or to quantify the exact value of the collateral that was included in the calculation of ecl ie.

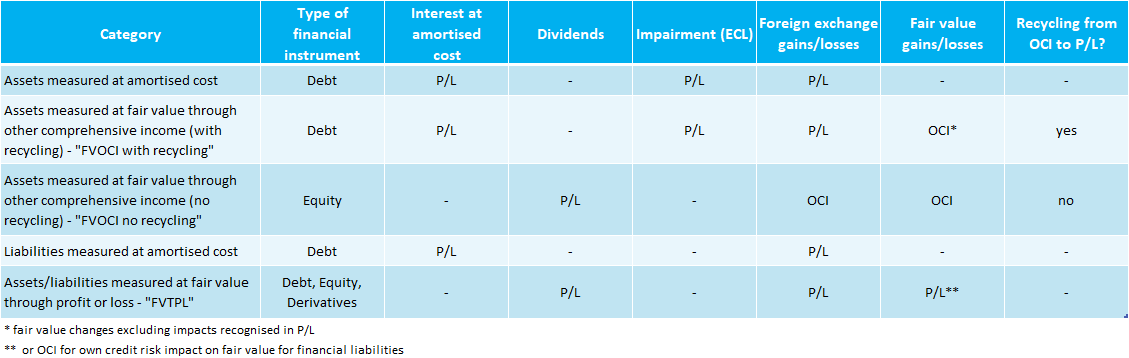

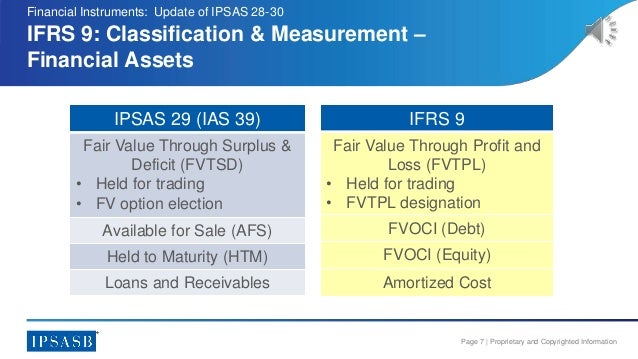

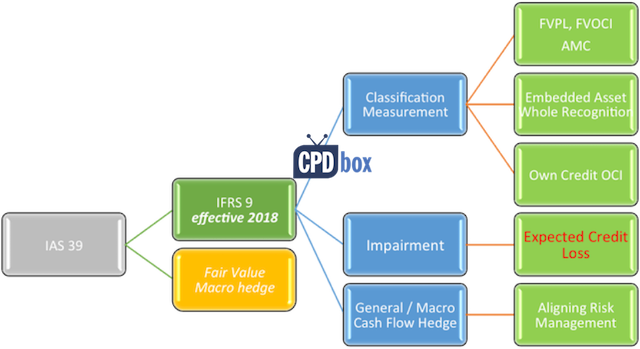

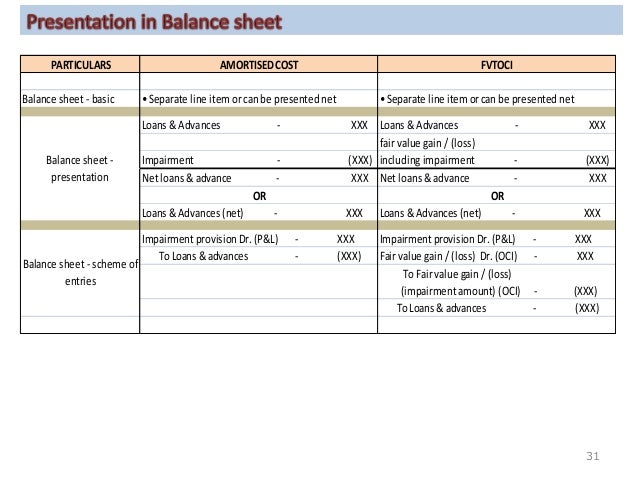

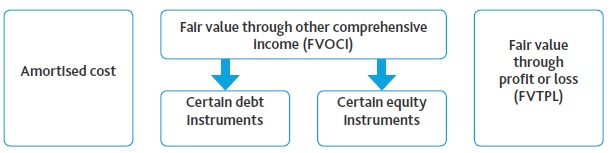

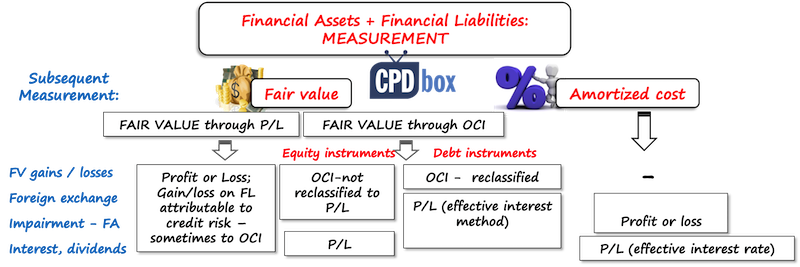

Fair value of loans ifrs 9. Liabilities measured at amortised cost. Under ifrs 9 all financial instruments are initially measured at fair value plus or minus in the case of a financial asset or financial liability not at fair value through profit or loss transaction costs. Subsequent measurement fair value with all gains and losses recognised in other comprehensive income changes in fair value are not subsequently recycled to profit and loss dividends are recognised in profit or loss. That is additional burden and completely different accounting because you have to set the fair value of such a loan at each reporting date which.

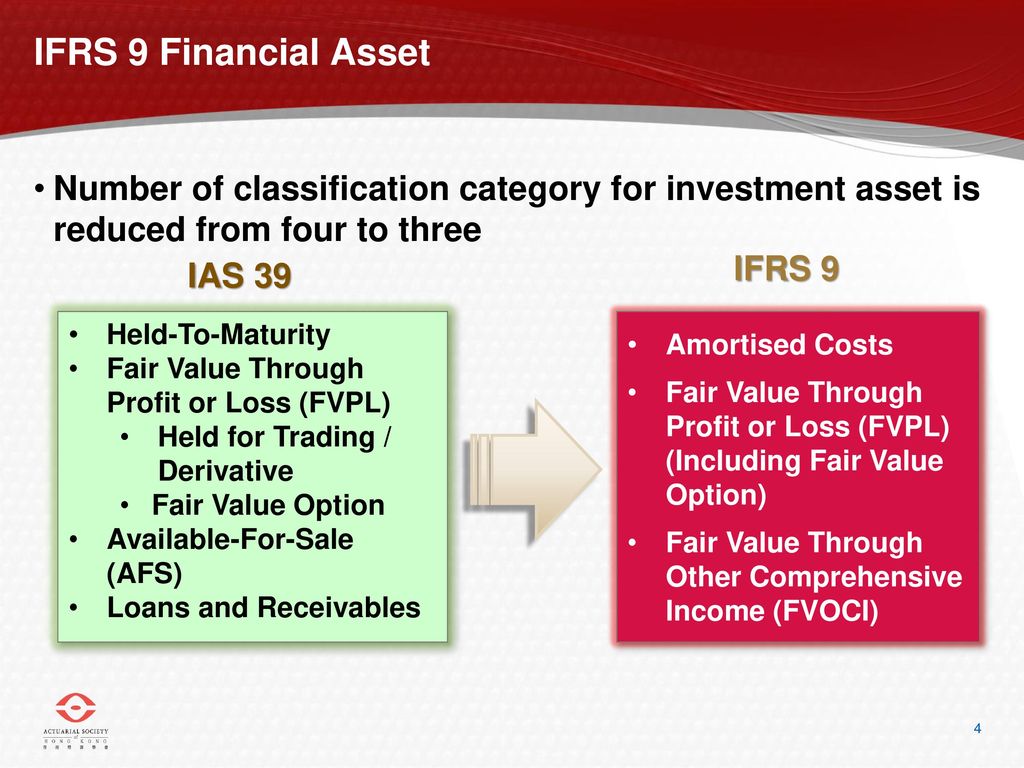

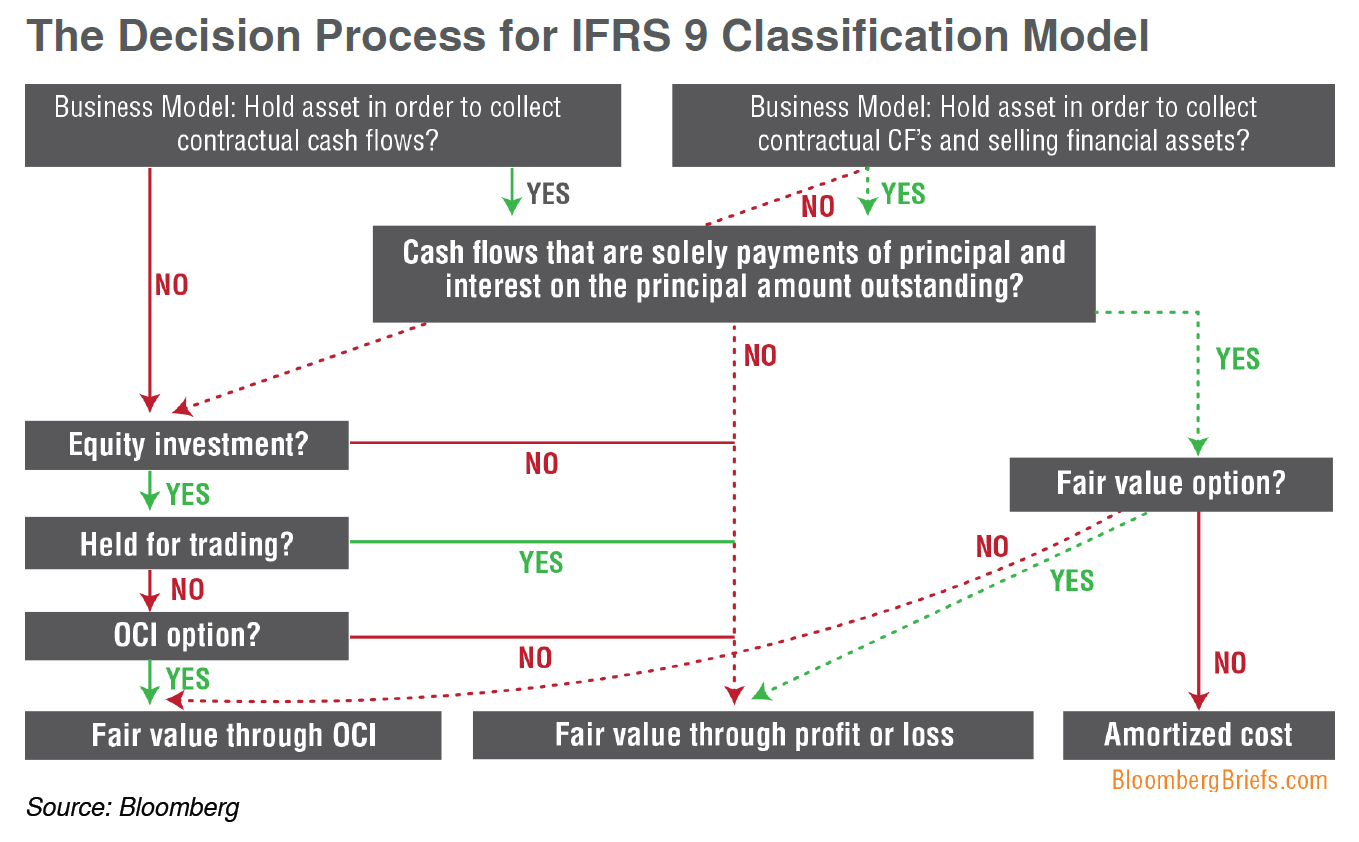

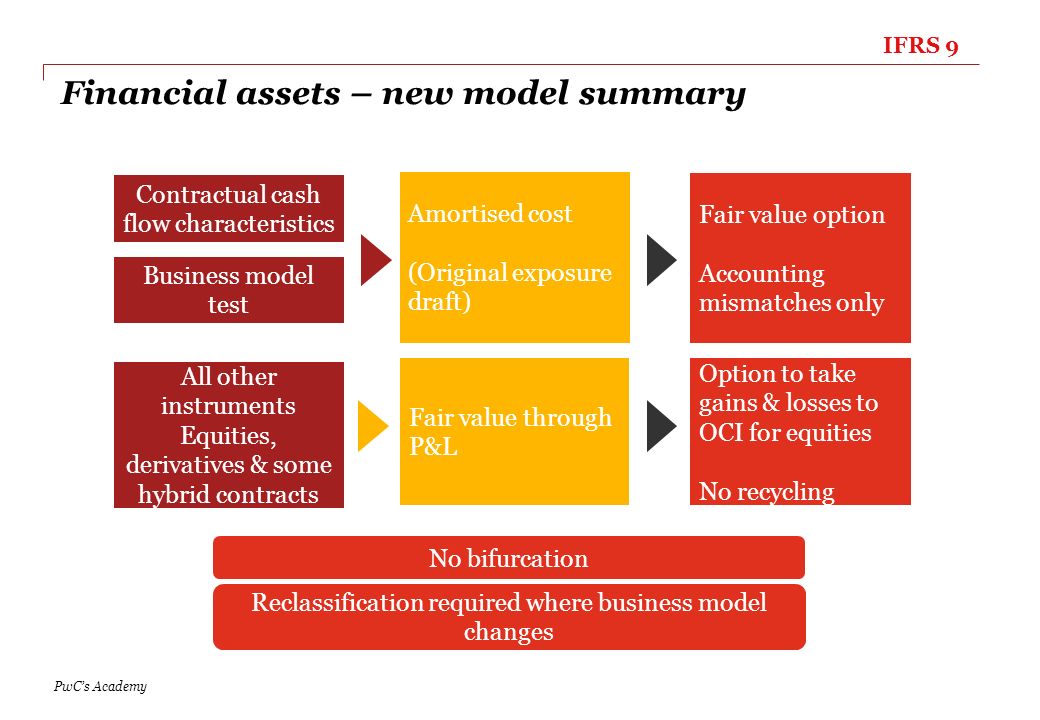

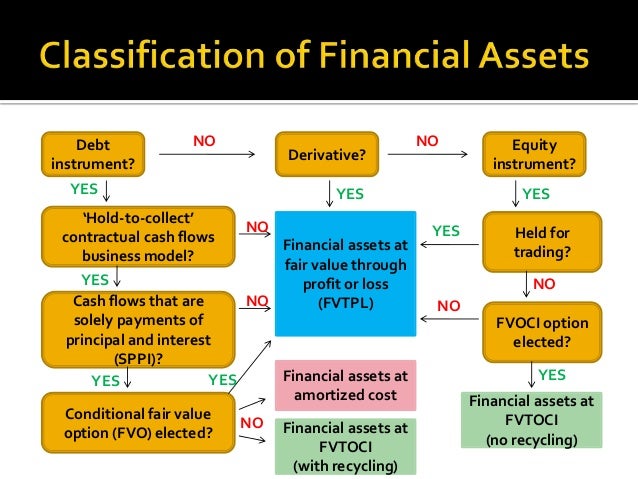

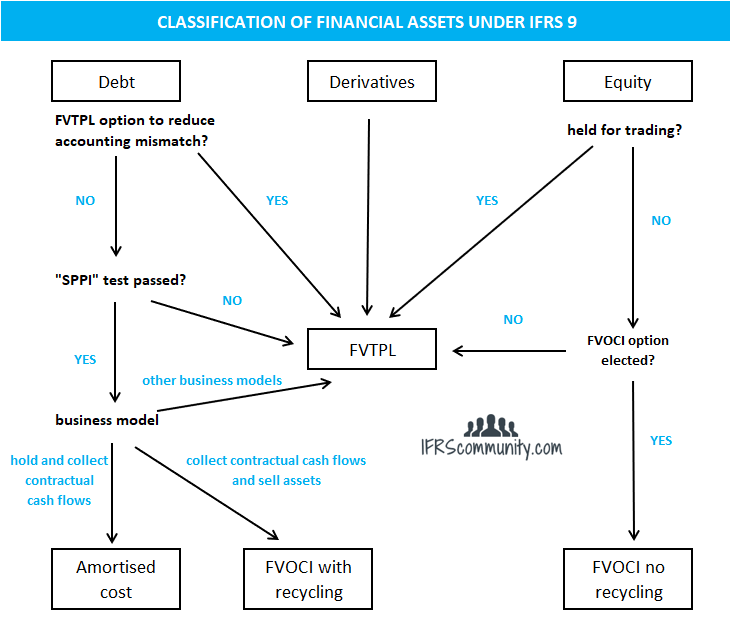

Debt instruments category classification criteria. Although accounting treatment of intercompany loans or financial liabilities under ifrs 9 financial instruments is almost same as discussed in our obsolete accounting standard ie. The standard defines fair value on the basis of an exit price notion and uses a fair value hierarchy which results in a market based rather than entity specific measurement. Within the scope of ifrs 9 that arenot held for trading.

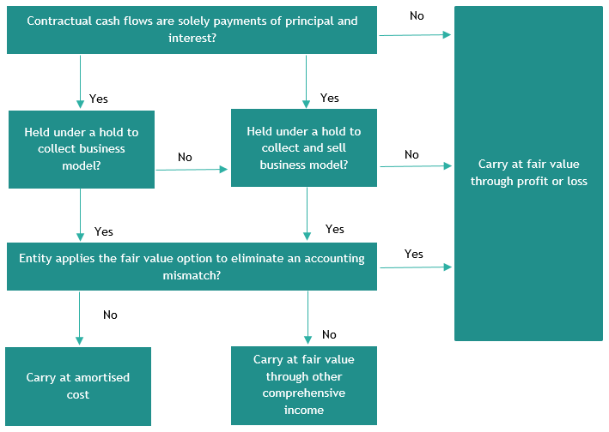

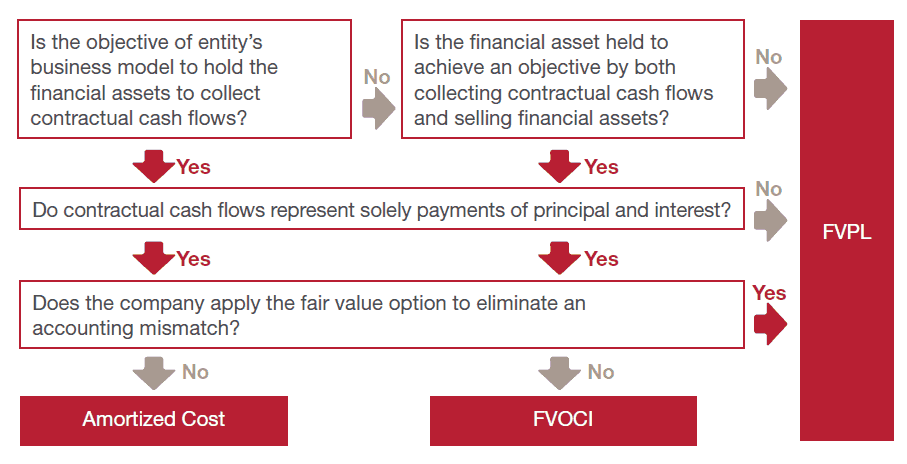

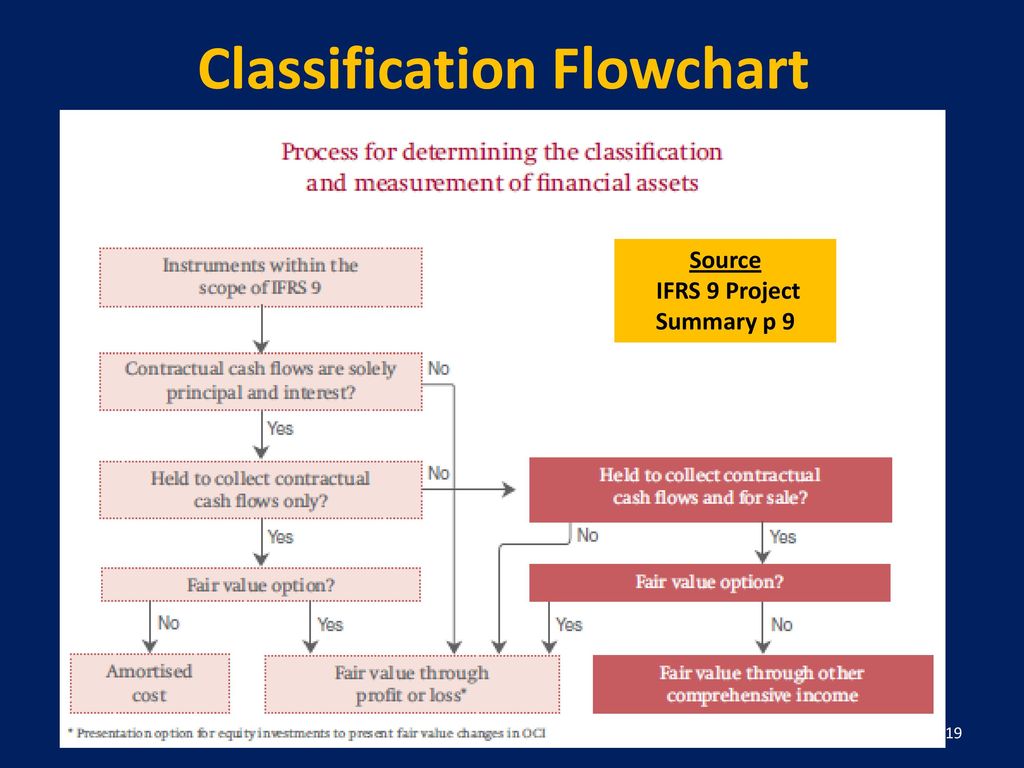

Such loans can be measured as the present value of all future cash receipts discounted using the prevailing market rates of interest for a similar instrument similar as to currency term type of interest rate. 6 disclosures under ifrs 9. Loans and receivables including short term trade receivables. Under ifrs 9 you can classify the loan at amortized cost only if it passes 2 tests.

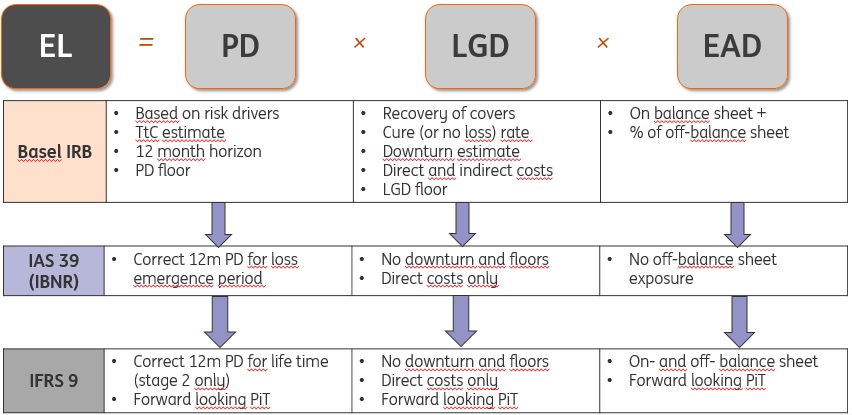

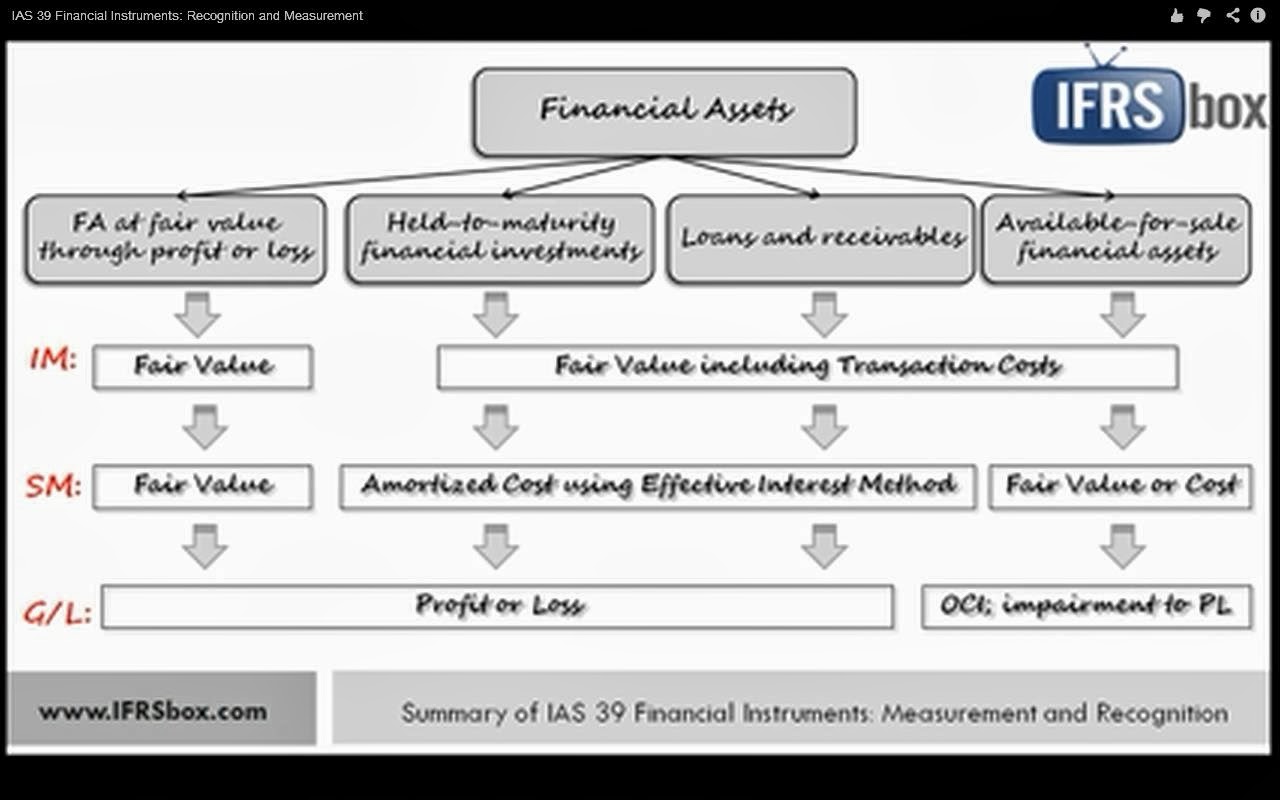

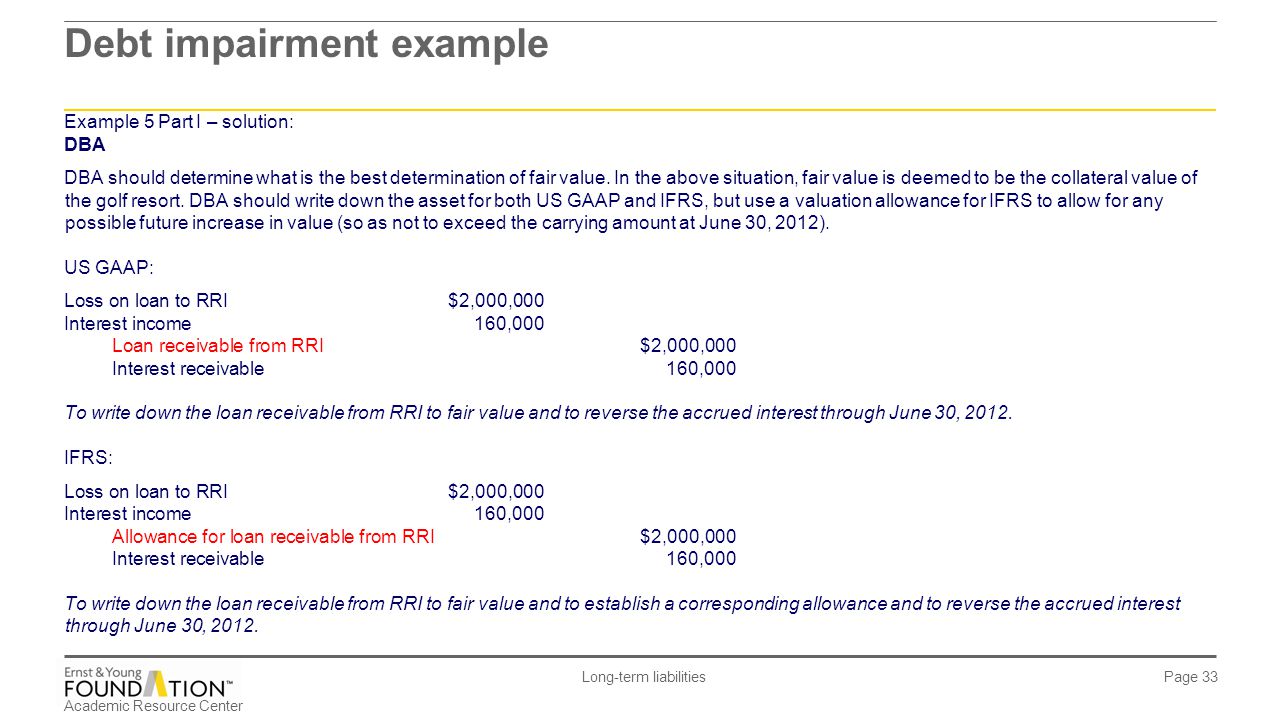

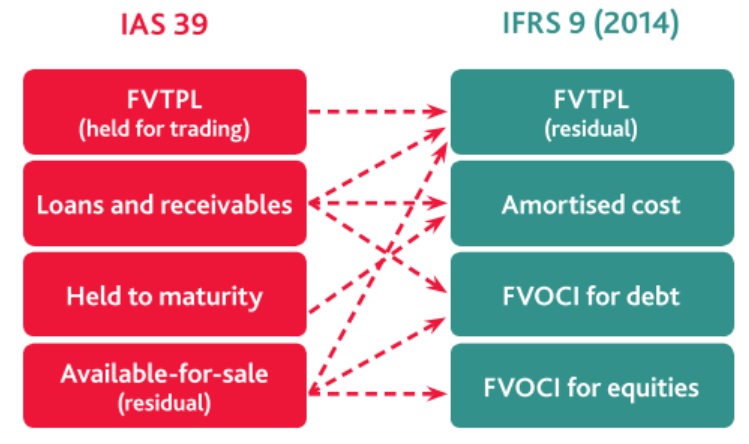

Ias 39 financial instruments. The loss given default lgd is not required. The difference between the fair value of the loan and the loan amount will be taken into profit or loss. This requirement is consistent with ias 39.

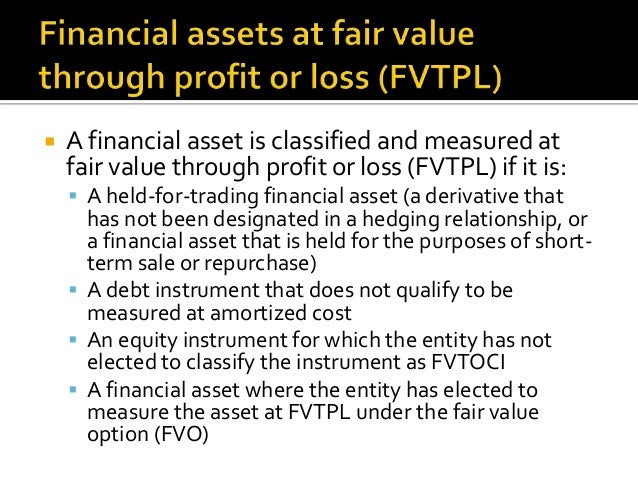

Cost as an estimate of fair value. Fvoci without recycling of fair value changes to profit and loss. On the other hand ifrs 9 establishes a new approach for loans and receivables including trade receivablesan expected loss model that focuses on the. In such a case no amortized cost but you have to classify the loan at fair value through profit or loss.

Although ifrs 9 requires all equity instruments to be measured at fair value it acknowledges that in limited circumstances cost may be an appropriate estimate of fair value for unquoted equity instruments. Ifrs 9 paragraph b511 provides guidance on determining the fair value of a long term loan or receivable that carries no interest.

Https Www Ey Com Publication Vwluassets Ey Ifrs Developments Issue 86 July2014 File Ey Ifrs Developments Issue 86 July2014 Pdf

Https Www Ey Com Publication Vwluassets Applying Ifrs E2 80 93 Ifrs 9 For Non Financial Entities File Applying Fi Mar2016 Pdf

Ifrs 9 The Sppi Test Explained By Example Annualreporting Info

Barco Annual Report 2017 By Barco Issuu

Ifrs 9 Financial Instruments Impairment Ey Fair Value Through

.jpg)